Blog Details

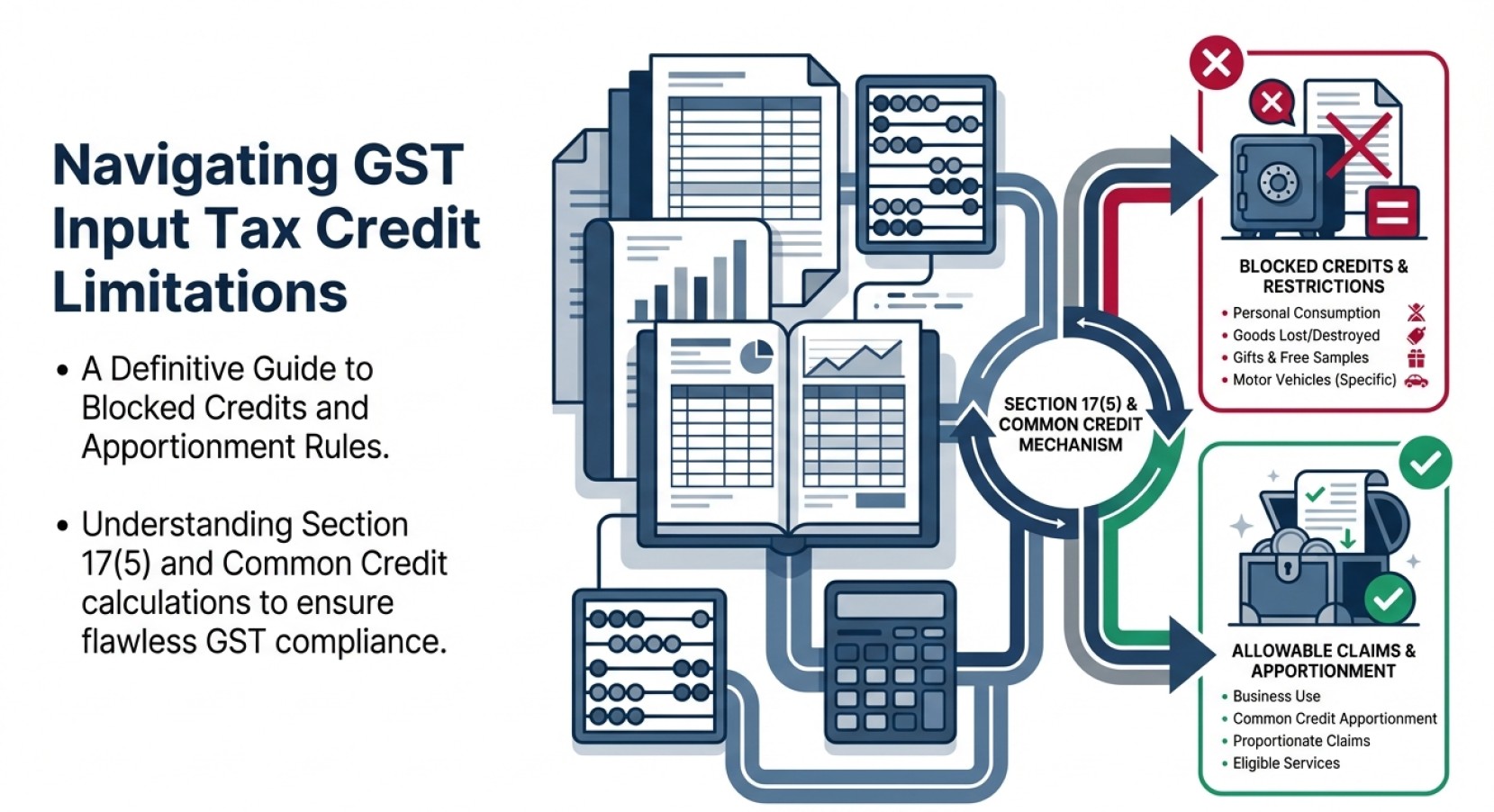

31. Blocked and Common Credits Under GST

When we talk about GST (Goods and Services Tax), one of the most attractive features for businesses is Input Tax Credit (ITC). In simple words, ITC allows you to reduce the tax you’ve already paid on purchases from the tax you owe on sales. Sounds neat, right?

But here’s the catch: not all taxes you pay can be claimed back as ITC. And this is where many businesses, especially beginners, get tripped up. GST has important restrictions. Some credits are blocked, and some must be shared or apportioned when a business deals with both taxable and exempt supplies.

Blocked Credits: When ITC Is Not Allowed

Blocked credits are expenses where ITC is not allowed, even if GST is clearly mentioned on the invoice. These are restricted under section 17(5) of the GST law because they are often personal or non-essential business expenses.

1. Motor Vehicles

Unless you’re in the business of transporting goods or passengers, ITC on cars is blocked. For example, if you buy a sedan for your company director, you can’t claim ITC.

2. Personal Use Items

Bought a laptop for your home but billed it under your business? Sorry, ITC won’t apply. ITC is only for business-related expenses.

3. Club Memberships & Recreation

Taking your team out for dinner? GST paid on that restaurant bill isn’t claimable. Membership fees for clubs, gyms, or recreational facilities are blocked.

Example:

A firm buys a corporate gym membership for employee wellness. Even if GST is charged, the company cannot claim ITC on it.

The government sees these as optional benefits, not essential business inputs.

4. Construction of Immovable

ITC is not allowed on goods or services used for constructing buildings (except plant and machinery). If you’re building an office space, ITC on materials like cement and steel is blocked. The idea is that once the property is ready, it becomes a capital asset, not a consumable business input.

This surprises many businesses because construction costs are huge. But GST law clearly blocks such credits.

Common Credits: When Expenses Serve Both Taxable & Exempt Supplies

Common credits arise when a business uses the same inputs for:

- Taxable supplies (GST is charged), and

- Exempt supplies (no GST is charged)

In such cases, you can’t claim full ITC. You must proportionately reverse the part related to exempt supplies.

Example: Business Selling Both Taxable and Exempt Goods

Consider a bookstore business that sells:

- Taxable items (like stationery and printed materials), and

- Exempt items like educational books

The shop pays GST on common expenses such as rent, internet or office supplies. Since these expenses support both taxable and exempt sales, you cannot claim full ITC.

- Instead, you must apportion the credit:

- Claim ITC proportionate to taxable supplies.

- Reverse ITC proportionate to exempt supplies.

Your business spends ₹10,000 on office rent with ₹1,800 GST.

- 60% of your turnover is taxable (stationery).

- 40% is exempt (educational books).

So, you can claim ITC only on 60% of ₹1,800 = ₹1,080. The remaining ₹720 must be reversed.

This ensures fairness — you don’t get ITC benefits for exempt supplies where GST isn’t charged to customers.

Why This Matters

Wrong claims can lead to penalties & interest. Knowing what’s blocked and how to apportion common credits keeps your compliance clean and stress-free.

Think of ITC like a buffet: you can enjoy most dishes, but some are off-limits. And if you try to sneak those onto your plate, you’ll be asked to pay extra at the counter!

Compiled by Ms. Amrin, Senior Audit Assistant - H M R R & Associates

Latest posts

Copyright | All Rights Reserved H M R R & Associates